It’s common for director shareholders to take additional remuneration in the form of dividends rather than bonuses. But with the corporation tax hike from April 2023 to 25%, would it be better to take bonuses instead in the 2023/24 tax year?

Historically dividends have been a more tax-efficient remuneration option than bonuses, particularly for those director shareholders with income in the higher and additional rate bands. However, there was a 1.25% dividend tax hike in April 2022 and April 2023 sees an increase in main corporation tax (CT) from 19% to 25% (profits under £50,000 will still be taxed at 19%). So, what does the combined impact of the rate changes mean to the effective tax rates for dividends compared with salaries?

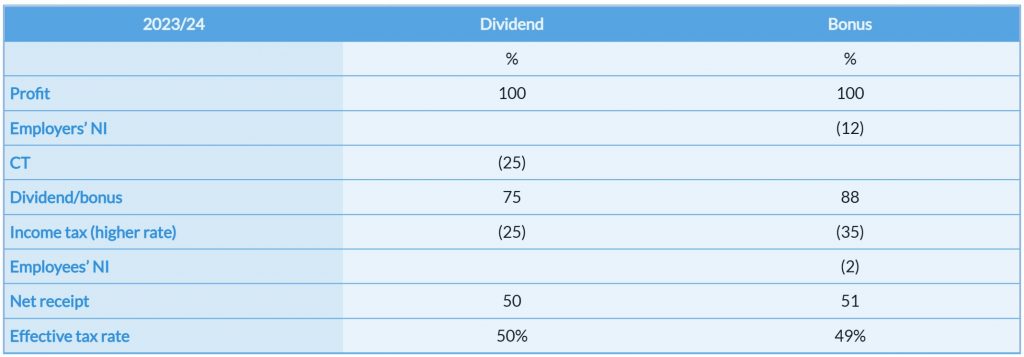

In the example below, I’ve assumed that the director shareholder has a salary above £50,270 so that any bonus will be taxed at the higher rate up to £125,140 and that the employees’ NI rate is 2%. The higher rate of tax on dividends is 33.75% and I’ve assumed a corporation tax rate of 25%.

The table shows that the effective tax rate for a higher rate taxpayer receiving a bonus that doesn’t take them into the additional tax rate band will be marginally better off receiving a bonus rather than a dividend.

Note: The above table doesn’t take into account the £1,000 tax-free dividend allowance which will reduce the effective rate of tax on dividends if the director shareholder doesn’t have any other dividends. For example, if the profits for the bonus were £15,000, the effective tax rate for dividends would be 48%, making it slightly better than a bonus so you’ll need to factor this into your calculations.

Additional rate taxpayer? I also calculated the effective tax rate for an additional rate taxpayer which was 54.51% for a dividend and 53.43% for a bonus.

Note: If the company’s profits are less than £50,000 and its CT rate remains at 19%, then it will be better to take a dividend rather than a salary.

There are, of course, other factors which should be taken into consideration as part of a director shareholder’s remuneration strategy, including:

1. If your company makes R&D claims, it may be even more beneficial to take an increased salary in order to maximise the R&D tax credit claim.

2. The timing of the tax payable will be different. Tax on a bonus is paid under PAYE and so is payable at the time whereas income tax on a dividend is paid on 31 January/July but will impact on payments on account.

3. Those director shareholders over state retirement age are not liable to pay employees’ NI and so will be even more better off taking a bonus.

4. There may be a benefit in taking a salary/bonus for pension contribution purposes as well as mortgage or other loan applications etc.

5. Pension contributions remain the most tax-efficient way to extract profits from a company for a director shareholder, assuming that you don’t need the money right now. But a director shareholder can only take a maximum of £40,000 a year as pension (although they can carry forward unused allowances for the previous three tax years).

In summary, the combined impact of the increased dividend tax and corporation tax means that the effective tax rates for dividends versus bonuses are expected to become broadly the same across each of the income tax bands. Therefore, whether to take a bonus or dividend will depend on other factors such as pension considerations, the availability of the dividend allowance and the age of the director.